- USD/MXN erases gains after positive Michigan Sentiment drives the US Dollar higher.

- The Mexican Peso remains vulnerable to broader risk sentiment, capping USD/MXN losses.

- US inflation moderates, but the Fed may not be willing to change its tone just yet.

The Mexican Peso (MXN) is showing renewed signs of weakness against the US Dollar after Michigan Expectations and Sentiment provided relief for the Greenback.

At the time of writing, USD/MXN is trading between the 19.30 and 19.40 psychological levels, with the 10-day and 20-day Simple Moving Average (SMA) providing additional support and resistance for the pair.

US Michigan sentiment data weighs on the Peso, limiting USD losses

The University of Michigan’s preliminary data for May, released on Friday, showed a modest improvement in consumer sentiment and expectations, offering a mixed but slightly more optimistic view of US household outlooks.

The Consumer Sentiment Index rose to 52.2, up from 50.8, indicating a small rebound in overall confidence. Meanwhile, the Consumer Expectations Index rose to 47.9 from 46.5, indicating that while consumers remain cautious about the future, their expectations have improved marginally.

Both readings remain historically low but point to a slight easing in pessimism, likely reflecting a stable labor market and slower inflation in recent months.

- Friday’s US Personal Consumption Expenditures (PCE) Price Index for April showed a MoM increase of 0.1%, slightly up from March’s unchanged rate. The YoY figure decreased to 2.1% from 2.3%. The core PCE rose to 2.5%, down from 2.7% in the previous month. This data suggests a dovish outlook for future US interest rates.

- The Federal Reserve’s (Fed) preferred inflation measure is closely monitored by policymakers, investors, and currency markets. Current data indicates that price pressures are easing, which influences expectations regarding future interest rates.

- In Mexico, the Jobless Rate for April, released at 12:00 GMT, printed at 2.5%, in line with analyst forecasts, despite a rise from 2.2% in March. Employment trends serve as a leading indicator of economic growth.

- The Banxico Minutes from the May Meeting on Thursday showed that most members see downside risks to economic activity; all members flagged concerns over US trade policy uncertainty. This reinforces a dovish bias from the central bank, with more easing potentially on the table.

- On Wednesday, Banxico’s Quarterly Report revealed that the central bank slashed its 2025 Gross Domestic Product (GDP) growth forecast to 0.1% from 0.6%, citing rising domestic recession risks. Market attention turns to policy calibration amid deteriorating growth outlook.

- The Minutes from the May Federal Open Committee (FOMC) meeting were released on Wednesday. In the report, Fed officials emphasized increased uncertainty and supported a cautious approach.

- USD/MXN remains highly sensitive to data surprises, especially when they carry implications for monetary policy or broader global sentiment. Price action is likely to be reactive, with potential for sharp swings should actual data deviate from expectations.

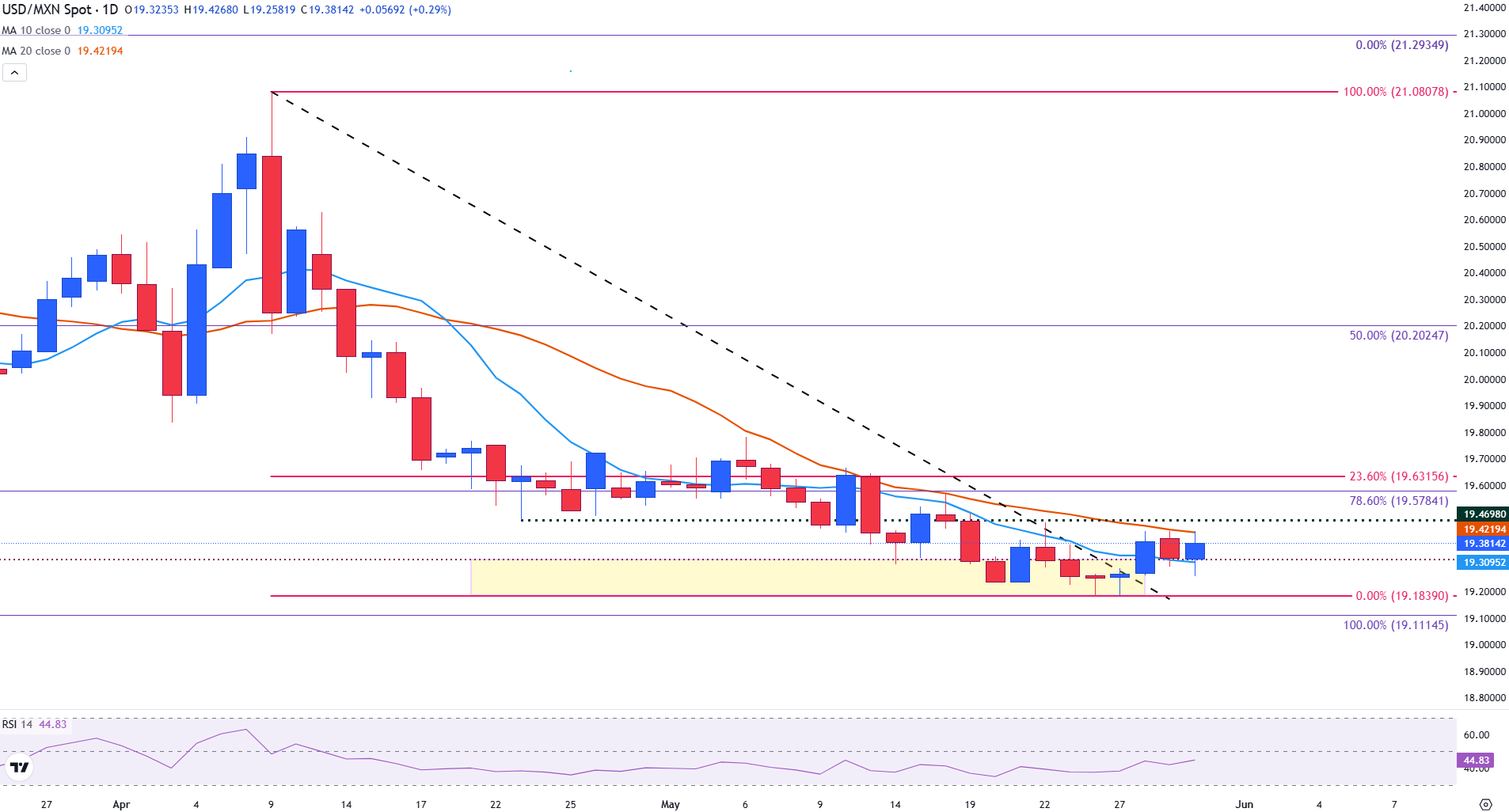

Mexican Peso technical analysis: USD/MXN bulls make a comeback

The USD/MXN is currently trading in a tight range between the 10-day Simple Moving Average (SMA) at 19.31 and the 20-day SMA at 19.42, reflecting indecision after a sustained downtrend.

A break above the 20-day SMA would bring the 78.6% Fibonacci retracement level of the October–February rally (near 19.58) into focus, and a successful move beyond that could open the door to the 23.6% Fib of the April–May decline around 19.63. The Relative Strength Index (RSI) has risen to 45, indicating that bearish momentum is fading, although it has not yet signaled bullish strength.

On the downside, a break below the 10-day SMA and psychological support at 19.30 would reassert bearish control, potentially pushing prices down to prior resistance at 19.28 and the May low at 19.18. This makes the current range a critical battleground for short-term direction.

USD/MXN daily chart

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.